Compare Life Insurance Quotes

Choosing the right life insurance can be overwhelming, especially with the wide array of options available in the market. One critical step in making an informed decision is comparing life insurance quotes. This guide aims to demystify the process of obtaining and comparing life insurance quotes, highlighting key characteristics of both term and permanent life insurance policies.

What is a Life Insurance Quote?

A life insurance quote is an estimated cost provided by insurance companies, detailing the potential expense of a life insurance policy. This estimate considers various factors such as the applicant's age, health, lifestyle, and the desired type and amount of coverage. Understanding life insurance quotes is crucial for individuals aiming to secure their financial stability and protect their loved ones.

Term Life Insurance

Term life insurance provides coverage for a set period, such as 10, 20, or 30 years. If the insured person dies during this term, beneficiaries receive the death benefit. It's often more affordable than permanent life insurance, making it a popular choice for those needing temporary coverage.

Permanent Life Insurance

Permanent life insurance, as the name indicates, provides coverage for the insured's entire lifetime, as long as premiums are kept up to date. This type of insurance typically includes a cash value component, which can grow over time and be accessed by the policyholder. While more costly than term life insurance, permanent life insurance offers lifelong protection and potential for financial growth.

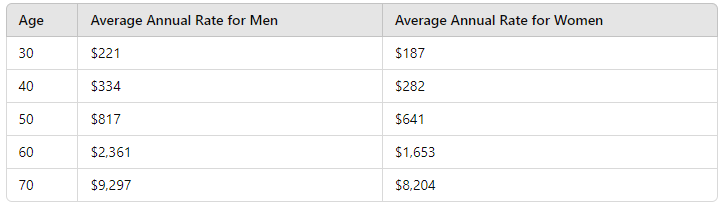

Comparing Life Insurance Quotes by Age and Gender

To clarify how life insurance quotes vary, let's examine the average annual rates for men and women across different age groups. The table below illustrates the latest data as of December 12, 2023:

(Source: Quotacy. Lowest three rates for each age and risk class averaged. Data valid as of December 12, 2023.)

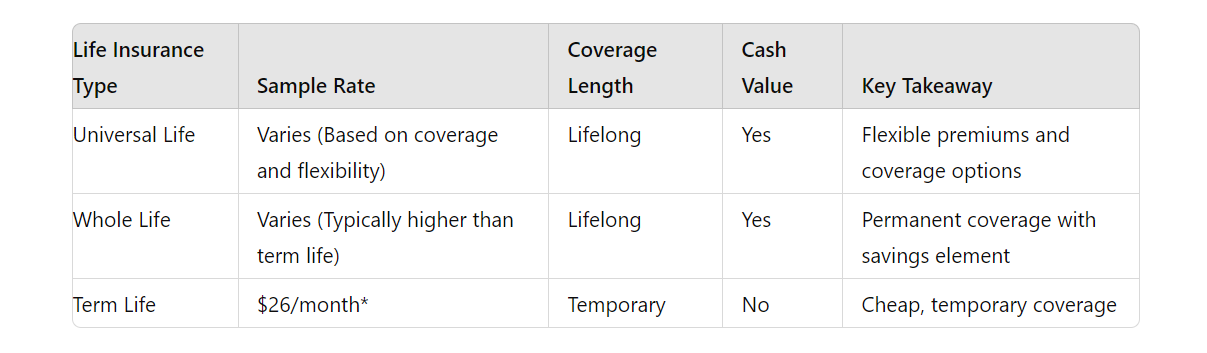

Comparison of Life Insurance Quotes

When evaluating life insurance quotes, it's crucial to grasp the distinctions between different policy types and their respective costs. Below are key considerations to help guide your decision, supported by current data.

(Information sourced from NerdWallet, Investopedia, and Policygenius. Data valid as of June 2024.)

*The term sample rate is based on a $500,000, 20-year term life policy for a healthy 40-year-old.

Term Life Insurance

Affordability: Term life insurance is generally the most cost-effective option. For instance, a $500,000, 20-year term life policy for a healthy 40-year-old costs about $26 per month. This makes it attractive for those seeking temporary coverage without a high financial commitment.

Coverage Length: The coverage is temporary, lasting for a specified term (e.g., 10, 20, or 30 years). After the term ends, the policyholder can choose to renew the policy at a higher premium or allow it to lapse.

Cash Value: Term life insurance policies do not build cash value. The premiums paid solely cover the death benefit, making it straightforward and cost-effective for those needing coverage for a specific period.

Key Takeaway: It offers affordable, temporary coverage ideal for young families, individuals with mortgage debt, or those seeking to ensure their loved ones' financial security during their lifetime.

Whole Life Insurance

Higher Premiums: Whole life insurance is generally more costly than term life insurance due to its lifelong coverage and the inclusion of a savings component that accumulates cash value over time.

Lifelong Coverage: Unlike term life, whole life insurance remains active for the insured's entire life, as long as premiums are paid. This guarantees that beneficiaries will receive the death benefit when the insured passes away.

Cash Value: One significant advantage of whole life insurance is the cash value component. Policyholders can borrow against this cash value or even surrender the policy for the cash amount, providing financial flexibility.

Key Takeaway: Whole life insurance suits those looking for permanent coverage and a savings element despite the higher cost. It's often used for estate planning and ensuring that heirs are financially secure.

Universal Life Insurance

Flexible Premiums: Universal life insurance offers flexible premiums and death benefits, allowing policyholders to adjust their coverage and payments as their financial situation changes. This flexibility can be beneficial but also requires careful management.

Cash Value Growth: Like whole life insurance, universal life policies have a cash value component. However, interest rates and the insurer's performance can influence the growth of the cash value.

Adjustable Coverage: Policyholders can often adjust the death benefit amount and premium payments. This can accommodate changes in financial responsibilities, such as paying off a mortgage or funding children's education.

Key Takeaway: Universal life insurance provides a blend of lifelong coverage and investment opportunities with greater flexibility. It's suitable for those who need adaptable financial planning tools and are comfortable managing their policy over time.

When comparing life insurance quotes, it's crucial to consider the cost and the type of coverage that best fits your needs. Term life insurance offers affordable, temporary protection, while whole life and universal life insurance provide permanent coverage with added financial benefits. Carefully evaluating these factors will assist you in selecting the appropriate policy to secure your financial future.

Find the Right Life Insurance Agents Near You

Securing the right life insurance policy is a significant decision; having the right guidance can make a substantial difference. Finding a knowledgeable and trustworthy life insurance agent can help you navigate through the various options and choose the best policy tailored to your specific needs.

Get a Life Insurance Quote Today

Types of Life Insurance Coverage

Understanding the various types of life insurance coverage is crucial for choosing the appropriate policy to suit your needs. The two primary categories of life insurance are term and permanent.

Term Life Insurance

Term life insurance covers a defined period, typically ranging from 10 to 30 years. If the insured person dies during the term, the beneficiaries receive the death benefit. Key features include:

- Affordability: Typically, term life insurance is the most affordable option, making it attractive for those on a budget.

- Simplicity: The policy is straightforward, with no cash value component. The premiums paid cover the death benefit only.

- Flexibility: Ideal for covering financial responsibilities that will reduce or end over time, such as a mortgage or children's education costs.

Permanent Life Insurance

Permanent life insurance offers coverage for the insured's entire life, provided that premiums are consistently paid. It includes various subtypes, including whole life, universal life, and variable life insurance. Key features include:

- Lifelong Coverage: Permanent policies remain in effect for the insured's entire life.

- Cash Value: These policies accumulate cash value over time, which allows policyholders to borrow against or withdraw from as needed.

- Investment Component: Some permanent policies offer investment options, allowing the cash value to grow based on market performance.

How Much Life Insurance Do I Need?

The amount of life insurance you need depends on several factors:

- Income Replacement: Calculate how many years your beneficiaries would require financial support by multiplying your annual income by that number.

- Debt and Expenses: Include the total amount of your debts, such as a mortgage, car loans, and credit card debt, plus future expenses like college tuition.

- End-of-Life Costs: Account for potential funeral and medical expenses.

- Existing Assets: Subtract any savings, investments, or existing life insurance coverage from your total needs.

A common rule of thumb is to aim for a death benefit that is 10-15 times your annual income, but individual circumstances can vary greatly.

How to Compare Life Insurance Quotes

When comparing life insurance quotes, take into account the following factors:

- Coverage Amount: Ensure the policy provides adequate death benefits to meet your needs.

- Policy Type: Decide whether term or permanent life insurance suits your situation.

- Premium Costs: Compare premiums to find an affordable policy that fits your budget.

- Riders and Options: Look for additional features or riders, such as critical illness or disability riders, that can enhance your coverage.

- Insurance Company Reputation: Choose a reputable insurer with strong financial ratings and positive customer reviews.

Where to Buy Life Insurance

There are multiple methods to purchase life insurance:

- Insurance Agents: Working with a licensed agent offers personalized advice and guidance through the complexities of various policies.

- Online Marketplaces: Platforms such as InsureHopper enable you to swiftly and effortlessly compare quotes from multiple insurers.

- Direct from Insurers: Some insurance companies offer the option to buy policies directly from their website or through their customer service channels.

- Financial Advisors: A financial advisor can incorporate life insurance into your broader financial plan and recommend policies that align with your goals.

Life Insurance Reviews

Reading life insurance reviews can offer valuable insights into the experiences of other policyholders. Consider the following sources:

- Consumer Websites: Sites like Consumer Reports and J.D. Power provide ratings and reviews based on customer satisfaction and company performance.

- Online Forums: Personal finance forums and social media groups can offer firsthand accounts of customer experiences with various insurers.

- Professional Reviews: Financial advisors and industry publications often review and compare life insurance products, highlighting their pros and cons.

By researching reviews and ratings, you can decide which life insurance policy and provider are best for you.

Applying for Life Insurance

Applying for life insurance can seem daunting, but understanding the process can make it much smoother. Here are the key steps involved:

- Determine Your Needs: Before applying, assess how much coverage you need and which type of policy is best for your situation. This involves considering your income, debts, future expenses, and financial goals.

- Compare Quotes: Use online comparison tools or consult with an insurance agent to gather quotes from different insurers. Compare similar policies to get an accurate sense of the costs and benefits.

- Complete the Application: Fill out the application form with accurate and honest information. This typically includes personal details, health history, lifestyle habits, and other pertinent information.

- Medical Exam: Many insurers require a medical exam to assess your health. This can include checking your height and weight, blood pressure, blood tests, and a review of your medical history.

- Underwriting Process: After the medical exam, the insurer's underwriting team reviews your application and medical results to determine your risk level and finalize your premium rates.

- Policy Approval: Once underwriting is complete, the insurer will approve or deny your application. If approved, you'll receive your policy documents outlining the coverage details and terms.

- Payment of Premiums: To keep the policy active, start paying your premiums as scheduled. Most insurers provide flexible payment options, including monthly, quarterly, or annual payments.

- Review and Update: It's important to regularly review your policy to make sure it still meets your needs, particularly after significant life events such as childbirth, buying a home, or marriage.

Comparing life insurance quotes is essential to finding the right policy for your needs. By understanding the distinctions between permanent and term life insurance, assessing how much coverage you need, and carefully comparing quotes, you can make a wise decision that ensures financial security for you and your loved ones.

For more personalized quotes and detailed comparisons, visit InsureHopper. Our platform provides a comprehensive tool to help you find the best life insurance policy tailored to your specific needs.

FAQs

Who Needs Life Insurance?

Life insurance is crucial for anyone with financial dependents, such as family members, as it serves as a reserve fund covering expenses like education costs, mortgage payments, and daily living expenses in case of your unexpected death. Even if you don't have dependents, life insurance can cover your final expenses and debts, averting them from becoming a burden to your loved ones after your passing.

What Is the Average Monthly Cost of Life Insurance?

The average monthly cost of life insurance varies widely depending on factors like age, health, type of policy, and coverage amount. For example, a healthy 40-year-old might pay around $26 per month for a $500,000, 20-year term life policy. Permanent coverages such as whole or universal life insurance are typically more expensive due to their lifelong coverage and cash value components.

What Is the Most Affordable Type of Life Insurance?

Term life insurance is normally the most affordable type of life insurance. It covers for a specific period, such as 10, 20, or 30 years, and does not accumulate cash value. This makes the premiums lower compared to permanent life insurance, which offers lifelong coverage and a savings component.